Jim Grant – Senior Product Insight & Technical Support Analyst

There’s sometimes confusion around what triggers the money purchase annual allowance. Find out what does and what doesn’t trigger the MPAA.

The money purchase annual allowance (MPAA) is a reduced annual allowance that can apply to contributions to defined contribution (DC) schemes.

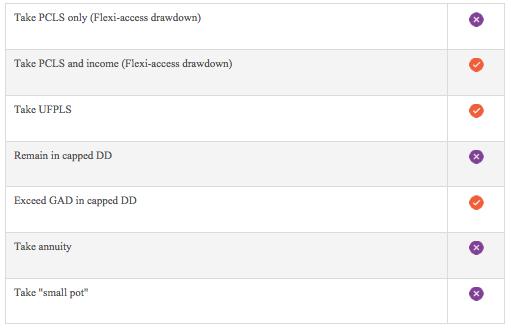

The following table covers what does and doesn’t trigger the MPAA.

When it was first introduced on 6 April 2015, the MPAA was set at £10,000. However, this was reduced to £4,000 with effect from 6 April 2017.

The important point is that the £4,000 limit applies to all those who have triggered the MPAA, including those who triggered it when it was £10,000. So someone who envisaged being able to continue contributing up to £10,000 p.a. will now face a charge if contributions exceed £4,000.

This issue is compounded by the fact that you can’t carry forward unused annual allowance or MPAA from previous years to pay more than the MPAA.

Another issue is how it affects the alternative annual allowance (AAA) for defined benefit (DB) savers. The MPAA only applies to DC savings; savers with both DC and DB savings benefit from the full annual allowance of £40,000 of which up to £4,000 may be paid into DC plans, leaving an AAA of £36,000 that applies to their DB rights if the MPAA is exceeded. Before the MPAA was reduced, the AAA was £30,000 if the MPAA was exceeded.

Clients should consider very carefully before taking income for the first time after 6 April 2017 and would definitely benefit from taking financial advice before they do.

Sources

- Reducing the money purchase annual allowance – Policy paper